Funding High - Impact Solutions for Basic Needs with Kevin Starr

Can unrestricted funding and radical trust unlock greater impact than traditional grants?

In this TBLI Talk, we sit down with Kevin Starr, CEO and director of the Mulago Foundation — one of the most respected and unconventional philanthropic organisations in the world. A former physician who stumbled into philanthropy in 1994, Kevin has spent three decades building a model that bets on the best people with the best ideas — and then gets out of their way.

Mulago finds, funds, advises, and promotes organisations with scalable solutions to poverty, working today with 50 portfolio organisations and 40 fellows across Africa, South Asia, and South America. Many of its portfolio organisations have become leaders in the global social sector.

In this episode:

What truly defines a high-impact organisation — and why most funders get it wrong

Why unrestricted, long-term funding produces better outcomes than traditional grant structures

The case for grants over investments — and when each is the right tool

How Mulago's eight-word mission statement framework helps social entrepreneurs design for measurable impact

Why measuring impact is not just about accountability — it is how organisations get better

The key insight: The social sector's biggest problem is not a lack of funding — it is a lack of rigour. The organisations that change the world are built around a big idea, designed for scale, and relentlessly focused on whether what they are doing is actually working.

👤 About Kevin StarrKevin Starr had a perfectly good career in medicine when he stumbled into philanthropy in 1994 — when his friend and mentor Rainer Arnhold died suddenly while the pair were working together in Bolivia, and Arnhold's family asked Starr to carry forward his legacy through the Mulago Foundation. Hewlett He completed medical school and residency at UC San Francisco. Mulagofoundation In 2003, he established the Rainer Arnhold Fellows Program to apply Mulago's principles and tools to help social entrepreneurs turn good ideas into lasting change at scale. Inspiringsocialentrepreneurs Mulago's portfolio includes globally recognised organisations such as One Acre Fund, Blue Ventures, Digital Green, Educate Girls, Noora Health, and Global Forest Watch. Kevin is a regular contributor to the Stanford Social Innovation Review and serves as chairman of Big Bang Philanthropy, a group of funders working to direct capital to those best at fighting poverty.

ABOUT TBLI RADICAL TRUTH Real experience. Real results. No greenwashing. TBLI Group is the world's leading ESG and impact investing network — educating, advising, and connecting investors for 25 years.

Most events are full of people handing you business cards they'll never follow up on.

TBLI Connect is different.

The people in this room aren't there to pitch you. They're there because they're genuinely curious, deeply experienced, and building something that matters. They'll challenge your thinking, open unexpected doors, and actually remember your name next week.

This is where careers accelerate — not because someone handed you a referral, but because you found your people.

One conversation at TBLI Connect can change your trajectory.

We've seen it happen. Every. Single. Time.

👉 Join us July 31st — seats are limited and they go fast.

If you're serious about surrounding yourself with the right people — not just successful people, but generous ones — this is the most valuable hour you'll spend this summer.

See you there. Tag someone who needs to be in the room. ⬇️

Why the TBLI Circle exists — and whether it's for you

Most networks are built for extraction. You show up, pitch yourself, collect contacts, leave. Nothing grows.

TBLI Circle was built on a different premise: that genuine people, connected to other genuine people, can actually move capital toward things that matter. We've been testing that premise since 1998.

The Circle is where those people go deeper.

It's not for everyone. But if you want to do serious work with serious people

Edited Chapter from my upcoming book Radical Truth. Extraction is a major theme of the book.

Last week I stood on a stage at an impact summit — surrounded by people using words like "stakeholder capitalism," "blended finance," and "net positive" — and said something that made a few people visibly uncomfortable.

I said: This is the same scam. Different logos. Different jargon. Different zip codes. But the same basic move.

I've spent more than thirty years in this space. I've watched the language evolve — from CSR to ESG to impact investing to regenerative capitalism — and I've noticed one thing that never changes: someone is always finding a new way to take something that belongs to everyone, or to the future, or to the earth, and convert it into a number that lands in someone's account.

They call it growth. They call it innovation. They call it fiduciary responsibility and disruption and, God help us, impact.

The rest of us should call it what it is: extraction.

The extraction economy isn't a bug. It's the operating system.

Walk through enough of the rooms — the finance conference, the business school, the consulting firm, the Silicon Valley pitch deck, the philanthropy gala, the ESG measurement workshop — and a pattern becomes impossible to ignore. In every single room, someone is running the same grift with a different business card.

The algorithm is just the latest priest. The MBA is just the latest credential for the con. The impact fund is just the latest way to feel virtuous while doing the same thing you were doing before.

I don't say this to be cynical. I say it because I've sat in those rooms. I've watched well-meaning people spend years building measurement frameworks that, in the end, gave cover to the thing they were supposed to challenge. I've watched the language of transformation get captured by the very system it was meant to disrupt.

Here's what frustrates me most: we actually know what works.

Not perfectly. Not painlessly. But we have the tools, the models, the evidence, and in some cases the money. We have practitioners around the world who are demonstrating — right now — what a genuinely regenerative economy looks like at the community level, the business level, the policy level.

What we are missing is not knowledge. It is honesty.

We are missing the willingness to say out loud what is actually happening — to stop pretending that the same system that built this mess is quietly going to fix it on a Tuesday afternoon. To stop letting new vocabulary serve as a substitute for new behavior. To stop rewarding the performance of change over the substance of it.

At the summit last week, someone asked me if I was being too harsh. Too negative. Wasn't I risking damaging the coalitions we've built?

I've heard that question for thirty years. And every time I hear it, the coalitions grow larger, and the extraction continues.

The hardest thing in this space is not finding the right framework. It's being willing to name the thing clearly — even when you're standing in a room full of people who have built careers on not naming it.

That's what I tried to do last week. That's what I'm trying to do here.

The extraction economy has many logos. It has one logic. And until more of us are willing to say that out loud — in the room, on the stage, on the record — the Tuesday fix is going to keep not coming.

What's the most honest thing you've said out loud in a room where it wasn't welcome? I'd like to hear it.

Anyone attempting to notch up a productive day’s work in the searing heat of southern England this last week was left in little doubt about the impact of extreme weather.

But the economic effects of the climate crisis for the UK are not confined to the many hours lost to quietly perspiring – or fetching kids dismissed early from scorching classrooms.

A pair of well-timed interventions from the finance lobby group TheCityUK and Swati Dhingra, the economist and independent member of the Bank of England’s monetary policy committee, made that point powerfully last week.

As Andy Burnham races towards No 10, both pointed to the need for a more active role for government in moderating the effects of the crisis in the years ahead.

TheCityUK’s report, written with the insurer Marsh, focused on the mounting challenge of insuring homeowners and businesses against the costs of extreme weather events.

With such events, including wildfires and floods, happening increasingly frequently and with growing severity, it argues that the risk of damage is becoming more difficult for insurers to price and warns of growing “protection gaps”.

It said: “Traditional actuarial methods – the basis for insurance pricing – assume the underlying probability of loss is broadly stable year to year. That assumption is becoming less reliable as climate hazards intensify, undermining the confidence with which insurers model expected future losses.”

That’s a tragedy for those affected, whose homes and livelihoods are left uninsured in the face of natural disasters.

But because of the important role of insurance in oiling the wheels of investment, TheCityUK argues that the difficulties of pricing climate risk will also have knock-on effects across the financial system. It is, they say, “not simply a sectoral issue, but a foundational concern for bankability, investability, and orderly economic activity”.

Of course, a financial lobby group has an interest in alerting us to the travails of the insurance sector, for which few are likely to shed a tear.

But they are right to warn that the unpredictability and severity of weather events is likely to be increasingly felt more widely.

And they say that could create a vicious cycle, in which too little is spent on adapting to climate risks, which increases the cost of climate damage and, in turn, raises the cost of investment, as insurers and lenders recoup their losses.

The report argues there is more that could be done by the private sector, for example, in developing ways to account for climate resilience in insurance. But it suggests there may also have to be more public – or partly public – backstops.

Dhingra’s speech points to another related vicious cycle. She highlights the increasing impact of adverse weather events worldwide, such as drought or excessive rainfall, on UK inflation.

As just one example, she says: “Chocolate alone contributed roughly 1 percentage point to UK food inflation in 2025, reflecting a surge in cocoa prices driven largely by extreme heat in west Africa and the fact that chocolate accounts for close to 6% of the UK food basket.”

In fact, further evidence for the impact of severe weather in our shopping baskets came in an analysis last week from the Energy and Climate Intelligence Unit, which found that 13% of UK food imports last year came from countries that are the least climate resilient, yet most exposed to extreme weather.

French energy giant TotalEnergies must identify and disclose measures to address climate risks resulting from Scope 3 greenhouse gas (GHG) emissions from the use of its oil and gas products, according to a new ruling by the Paris Judicial Court.

The order gives the company six months to update its legally mandated vigilance plan to integrate the Scope 3 considerations and measures, which the court will review when the proceedings continue early next year.

In a partial victory for TotalEnergies, the court did not mandate specific emissions or oil and gas production reduction targets, or set requirements for the company to stop new fossil fuel-related exploration activity, as requested by the organizations behind the lawsuit.

The suit was initially filed in 2020 by a group of NGOs including Notre Affaire à Tous, Sherpa, France Nature Environnement, and the City of Paris, following France’s adoption of its “duty of vigilance” law in 2017, requiring large companies to have a vigilance plan to assess and prevent their operational impacts on the environment and human rights.

In the suit, the organizations argued that TotalEnergies’ vigilance plan was incomplete, by not sufficiently incorporating the climate-related risks and harms resulting from its activities, and particularly from the GHG emissions resulting from the combustion of fossil fuel products, which represent nearly 90% of the company’s GHG footprint.

The suit asked the court to set a series of requirements for TotalEnergies in its plan, including identifying its contribution to global GHG emissions and climate change risks, publishing measures to align its activities with a GHG emissions pathway – including Scope 1, 2 and 3 emissions – compatible with limiting global warming to 1.5°C, and requiring the company to set interim targets to reduce the carbon intensity of its products in line with the 1.5°C pathway, to reduce natural gas and oil production by specific amounts by 2030 and 2050, as well as to immediately halt new hydrocarbon exploration.

In its judgement, the court ruled that climate-related risks to which the company contributes through its activities fall within the scope of the vigilance law, and that TotalEnergies must identify the adverse climate impacts caused by the release of GHG emissions resulting from its activities in its risk mapping.

The court added in its ruling that emissions from the company’s activities include Scope 3 emissions, in particular due to the “inherent link between oil and gas production and the combustion of the products by end users.”

The court ruled that TotalEnergies plan is incomplete without Scope 3 emissions, and ordered the company to complete the plan within 6 months, with Scope 3 added to its risk mapping, along with related measures corresponding to the risks.

In a statement welcoming the ruling, the coalition behind the suit said:

“This is an important decision during these days of unprecedented heatwave: fighting climate change is also fighting for a livable future. Multinationals – particularly oil and gas companies like TotalEnergies – must do their part to protect our loved ones, the regions we cherish, and those most vulnerable to the effects of climate change. We will continue the fight to ensure that this is the case.”

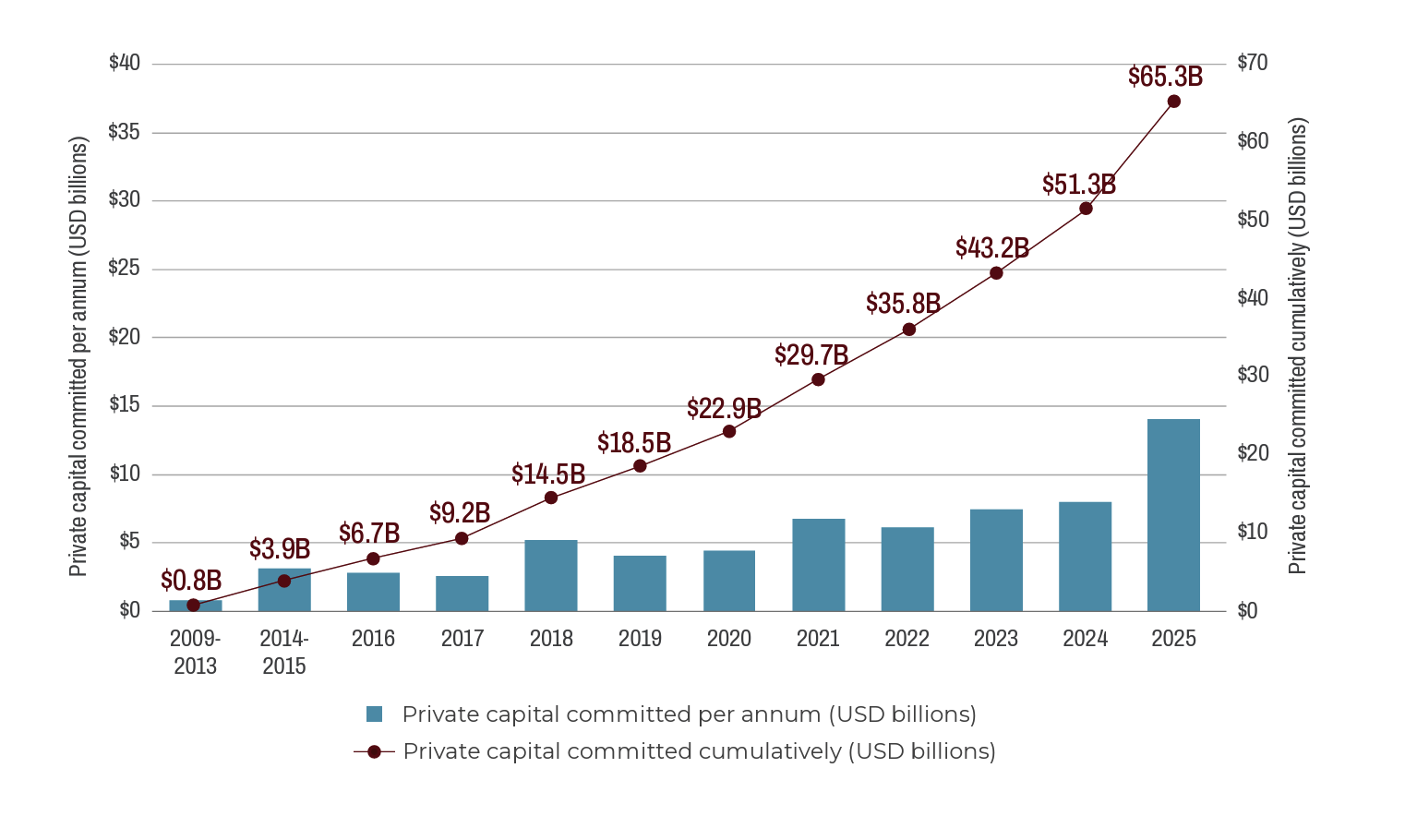

New comprehensive analysis from The Nature Conservancy and Forest Trends explores global private capital flows to nature

ARLINGTON, Va., June 22, 2026 /3BL/ - As climate change and biodiversity loss intensify, protecting and restoring nature is increasingly recognized as essential for environmental and economic resilience. A convergence of structural, market, and policy forces is bringing nature-related risks and opportunities into sharper focus for the private sector, driving increased interest in investing in nature-based solutions.

But as attention and ambition grow, a key question remains: is private capital translating that momentum into real investment on the ground, and at the scale needed?

Building on a benchmark series first published in 2014, the analysis draws on more than a decade of global data tracking private capital flows to nature. Based on 1,731 transactions from 2016–2025 and survey data from 70 institutions representing $207 trillion in AUM, the report combines survey outreach, desk research, and public data sources.

The findings point to a field that has expanded significantly in both scale and complexity, shaped by growing recognition of nature-related risks and opportunities, evolving financial models, shifting macroeconomic conditions and strengthening policy signals.

Key findings include:

Private investment in nature has grown significantly, with more than $60 billion deployed over the past decade. Annual flows have increased fivefold, from $2.8 billion in 2016 to over $14 billion in 2025, and over $180 billion in private capital is targeted for the years ahead, underscoring accelerating momentum.

More than half of flows were to working landscapes like sustainable agriculture and forestry, where nature is the critical infrastructure underpinning food production, forest products, water security, and responsible commodity supply chains.

Private investment is heavily concentrated in the Americas, with Latin America alone attracting over $15 billion over the last decade, while regions like Africa and Asia remain significantly underfunded despite their critical ecological importance. The gap reflects the importance of policy enablers and market conditions for investment readiness.

Institutional, return-first investors increasingly view nature investments as financially competitive, with 88% of surveyed investors reporting a positive relationship between financial returns and impact. A growing trend toward financial risk-reducing approaches, including the use of public and philanthropic funding to bring in private capital —engaged by two in three respondents—and integrated models that combine multiple revenue streams, is helping attract these types of investors to the space.

Private capital committed to nature investments, 2009–2025

Source: Forest Trends’ Ecosystem Marketplace and The Nature Conservancy, Gaining Ground: State of Private Investment in Nature 2026

Photograph: Tolga Akmen/EPA

Photograph: Tolga Akmen/EPA