Welcome to TBLi Radical Truth Podcast, where knowledge inspires and we explore innovative investment models democratizing impact investing, sustainable finance, and climate solutions. In this episode, we're joined by Ellen Hensbergen, Managing Director Benelux at Invesdor—Europe's leading impact crowdfunding platform. With leadership experience at ABN AMRO and Munt Mortgages, Ellen is pioneering a financial revolution in impact capital and equity crowdfunding, shifting from exclusive venture capital to a pan-European ecosystem where everyday investors fund renewable energy, sustainable startups, and UN Sustainable Development Goals-aligned climate solutions.

In "Democratizing Impact Capital Through Crowdfunding," Ellen reveals how Invesdor's merger with Oneplanetcrowd created Europe's largest impact investment platform. From renewable energy projects like Windpark Fryslân to MedTech and circular economy innovations, she demonstrates how equity crowdfunding bridges financial returns with measurable social impact and ESG performance. Ellen shares how the European Crowdfunding Service Provider (ECSP) license enables cross-border impact investing across Europe, why crowdfunding is becoming a viable alternative to traditional VC for sustainable startups, and how transparent impact measurement tracks environmental and social returns alongside financial performance.

TBLi Radical Truth Podcast brings you leaders in sustainable finance and ESG who are democratizing capital markets for climate action. Let's begin our conversation with Ellen Hensbergen on impact crowdfunding and sustainable investing in Europe. This is TBLi Radical Truth Podcast.

8:00 AM - Continental Breakfast (stale pastries, weak coffee) 8:30 AM - Keynote: "The Future Is Now" (it's not) 10:00 AM - Panel: People Who Agree Agreeing 11:30 AM - Networking Break (stand awkwardly, check phone) 12:00 PM - Lunch (rubber chicken returns) 1:30 PM - Workshop: Learn things you could've Googled 3:00 PM - Another Panel: More Agreement 4:30 PM - "Speed Networking" (17 minutes of chaos) 5:00 PM - Closing Remarks: "Let's stay in touch!" 5:15 PM - Everyone immediately forgets everyone

COST: $2,500 + travel + hotel + soul

TBLI VIRTUAL MIXER AGENDA:

16:00 CET - AI matches you with impact investors you ACTUALLY need to meet 16:00-17:30 - Have real conversations about real deals 17:30 - Done. No travel. No bad food. No pretending.

All contacts made are shared immediately after with their contact details.

COST: Your time and attention (that's it)

Friday, Feb 27, 16;00 - 17:30 CET

The best deals happen in the right conversations. This is where those conversations happen.

Without the rubber chicken. Without the extraction.

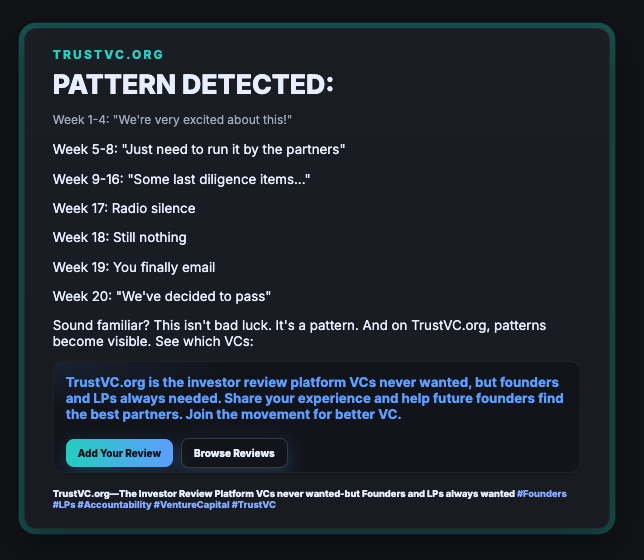

Week 1-4: "We're very excited about this!" Week 5-8: "Just need to run it by the partners" Week 9-16: "Some last diligence items..." Week 17: Radio silence Week 18: Still nothing Week 19: You finally email Week 20: "We've decided to pass"

Sound familiar?

This isn't bad luck. It's a pattern.

And on TrustVC.org, patterns become visible.

See which VCs: 🚩 Consistently ghost founders 🚩 Change terms at the last minute 🚩 Over-promise and under-deliver ✅ Actually respond promptly ✅ Honor their commitments ✅ Support founders through challenges

One founder's experience is anecdotal.50 founders reporting the same thing? That's data.

Your months are too valuable to waste on VCs with bad patterns.

Last spring, the Environmental Protection Agency made a surprise announcement: President Donald Trump would consider giving some polluters exemptions from a handful of Clean Air Act rules. To get the ball rolling, all it would take was an email from a company making its case. The EPA set up a special inbox to receive these applications, and it gave companies about three weeks at the end of March to submit their requests for presidential exemption. Hundreds of companies wrote in, including coal plants, iron and steel manufacturers, limestone producers, and chemical refiners.

One industry was particularly eager for exemption: medical device sterilizers. About 40 of the roughly 90 device sterilization plants that operate nationwide, along with their trade association, wrote in, arguing they shouldn’t have to comply with an air quality rule limiting how much toxic material they could emit. That’s because these facilities sterilize medical equipment with ethylene oxide, a potent carcinogen that studies have linked to cancers of the breast and lymph nodes.

In 2024, the Biden administration issued regulations requiring sterilizers to cut their emissions by about 90 percent. Companies were given two years to comply, and many had begun installing new monitoring equipment and pollution-control devices to meet the standard. But last year, after President Trump took office, the EPA gave these companies a way out; they could request a presidential exemption. About 40 facilities, many of which are located in residential neighborhoods close to schools and day cares, took advantage of the offer and were granted the exemption through a presidential proclamation last summer.

Now, a coalition of national environmental groups and community nonprofits is suing Trump and the EPA, seeking to overturn the ongoing exemptions. Maurice Carter, president of the Georgia-based environmental advocacy group Sustainable Newton, which signed on to the suit, told Grist that financial interests of sterilization companies shouldn’t override public health concerns about ethylene oxide. Any policy change should account for that, he argued.

“You have to do that in ways that are not harmful to the people that live here and to the planet that our children are going to inherit,” he said. Carter lives about a mile away from one of the exempted facilities.

This B Corp Asia Summit 2026 brings together thought leaders and practitioners to showcase the emerging trend that Business as a FORCE for Good is Good for Business.Global MNCs, as well as Asian SMEs share how incorporating positive impact on how you run your business translates into financial success.

Transition-labelled bonds are anticipated to emerge as the fastest-growing segment of the sustainable bond market in 2026, driven by demand for instruments to finance decarbonization strategies in hard-to-abate sectors and the availability of new standards to define eligible investments, according to a new sustainable finance market forecast released by Moody’s Ratings.

Overall, the report forecasts the issuance of labelled sustainable bonds – including green, social, sustainability, sustainability-linked, and transition bonds – to remain roughly flat year-over-year at $900 billion, after falling in 2025 following four consecutive years with issuance above $1 trillion.

Key drivers supporting sustainable bond market issuance in the coming year identified by the report include a focus on sustainable financing to address material climate mitigation and adaptation investment gaps, which will continue to be offset by political headwinds in some markets, as well as competing investment priorities such as energy security and defense.

Moody’s noted as well that issuance may be supported by outsized volumes of maturing labelled bonds, estimating that approximately $520 billion of labelled bonds have a 2026 maturity date, compared with $425 billion last year.

By bond type, the report forecasts that green bonds will continue to dominate the market, representing nearly 60% of issuance at $530 billion, and roughly flat with last year, followed by sustainability bonds – which combine green and social projects – at $190 billion, social bonds at $155 billion, and $40 billion for transition bonds, while sustainability-linked bonds (SLBs) will remain subdued at around $25 billion, down from record issuance of $96 billion in 2021, with SLBs continuing to be pressured by scrutiny of their target ambitions by investors.

While remaining a small component of the overall market, the report anticipates that transition bonds, which finance climate transition projects that substantially reduce or avoid emissions at high-emissions activities that may not qualify for a green label. In addition to growing demand for labelled instruments to help channel capital into decarbonization strategies in hard-to-abate sectors, the report anticipates issuance will be supported by the new availability of new standards and guidelines providing criteria and safeguards for use of capital for investors. Notably, several new and in-development sustainable investment taxonomies now include transition categories.

The report forecasts transition bond issuance growing to $40 billion, nearly double the record issuance of $21 billion reached in 2024.

India’s Economic Survey 2025–26 reframes climate action as a development-first strategy, placing adaptation, resilience, and human welfare at the centre of policy design.

Domestic adaptation and resilience spending rose from 3.7 percent of GDP in FY16 to 5.6 percent in FY22, underscoring India’s reliance on internal capital rather than external climate finance.

Non-fossil fuel sources now account for 51.93 percent of installed power capacity, while critical minerals, nuclear reform, and carbon markets reshape India’s energy and finance architecture.

A Development Lens on Climate Policy

India’s climate strategy is being recalibrated around development realities rather than abstract emissions targets, according to the Economic Survey 2025–26 tabled in Parliament by Union Minister for Finance and Corporate Affairs, Smt Nirmala Sitharaman.

“The global climate change agenda has reached an inflexion point,” the Survey states, adding that what was once framed as a moral and technological transition toward net zero is now defined by trade-offs, capacity constraints, and a widening gap between ambition and operational reality. It cautions that introducing complex systems too quickly, without buffers or institutional capacity, risks fragility rather than resilience.

The Survey’s core argument is explicit: climate policy must prioritise human welfare, particularly for poorer and climate-vulnerable societies, and development itself should be recognised as a form of adaptation.

Adaptation Anchored in Growth

India’s adaptation strategy is embedded in public investment across agriculture, water, urban infrastructure, and social systems. Domestic spending linked to adaptation and resilience rose from 3.7 percent of GDP in FY16 to 5.6 percent in FY22, a scale rarely matched among emerging economies.

The National Action Plan on Climate Change operates through nine missions, many focused on climate resilience. These include climate-resilient agriculture, integrated water management, and ecosystem protection. State Action Plans on Climate Change translate national priorities into local policy, a critical function as urbanisation accelerates and climate risk increasingly shapes land use, infrastructure planning, and service delivery.

The Survey emphasises that adaptation is not a separate climate pillar but a structural feature of India’s growth model.

Energy Transition as a System Strategy

On mitigation, the Survey warns against treating energy transition as a narrow climate exercise. Sustained growth and rising living standards require a large expansion of affordable, reliable electricity. Renewable capacity additions alone do not guarantee dependable supply.

India’s approach blends renewable expansion with nuclear power, green hydrogen, battery storage, and grid stability investments. By December 2025, non-fossil sources accounted for 51.93 percent of installed capacity, exceeding India’s earlier targets.

The Survey contrasts this measured approach with European experiences where transitions outpaced investments in baseload generation and system flexibility, resulting in price volatility and supply risks. Material availability and storage constraints remain binding challenges for India’s clean energy scale-up.